VIEW FROM THE TOWER

Should we Party Like It’s 1999?

By Mike Horwath, CFA · Chief Investment Officer

For the inaugural post, I thought an ode to our founder, Matt Topley, was in order. Matt’s quarterly

commentary — which takes its title and direction from a song — is a genuinely informative read, and one

I’d recommend to anyone interested in markets.

The ’90s gave us the buildup to Y2K, the explosion of grunge (Alice in Chains’ 1996 MTV Unplugged set is a

personal favorite), and a frenzy of technology IPOs (initial public offerings). With the recent IPO of SpaceX

— and the anticipation that Anthropic and OpenAI follow this year — we’ve fielded plenty of questions

about what it all means for individual portfolios, and whether it’s worth buying shares if the opportunity

arises. There’s a lot of noise out there, so I thought it would be worthwhile to dig into what this means,

and to share our perspective here at Lansing Street.

How did we get here?

Outside of the SPAC (special purpose acquisition company) nonsense of 2021, the IPO market has been relatively quiet since 1999 — the year companies like Nvidia, UPS, Goldman Sachs, and BlackRock made their debut. Despite the growth of the overall stock market, the number of publicly traded companies has steadily declined over the past few decades. One reason: many smaller companies have either stayed private or gone private to sidestep the regulatory burden that comes with being public. At the same time, the amount of private equity capital flooding the market has looked parabolic. At the end of 2023, the number of private-equity-backed companies was 2.5x the number of public companies.

These forces have combined to create very large businesses owned by founders, venture capital, and private equity. One challenge of staying private this long is that investors eventually want to monetize their returns and diversify away from a concentrated position. That brings us to 2026, when this group of mega-cap companies has finally decided to shift from private to public ownership.

Size over volume.

What makes 2026 so different from 1999 is that we’re seeing roughly the same percentage of total market capitalization come to market — but through only three businesses. The sheer size of these companies, and what they mean for markets, is on a far different scale than what we saw in 1999.

In hindsight, the tech bubble of 2000–2002 was predictable given how many IPOs came to market with no revenue at extreme valuations. Hindsight is always 20/20. The fundamentals for SpaceX, Anthropic, and OpenAI have come under similar scrutiny, though at different scales. At valuations (or expected valuations) of roughly $1.75 trillion, $1 trillion, and $1 trillion, respectively, many investors are asking what the real path to profitability looks like.

For perspective, Meta’s market capitalization is roughly $500 billion less than SpaceX’s as of the end of June 2026. Meta has billions of daily active users, nearly 9x the annual revenue, and $70 billion of operating income — versus a $2+ billion loss for SpaceX. By every fundamental measure, Meta should be worth more. Markets can be funny that way.

The key isn’t where we’ve been, or even where we stand today, but where investors think we’re going. During the SpaceX roadshow, Goldman Sachs projected revenues climbing from $18.7 billion in 2025 to $474 billion in 2030 on the back of AI-related demand. Now, Goldman isn’t the most unbiased party in this conversation, so take that with a grain of salt. Either way, investors are buying potential growth — across AI for all three businesses, and space launch and satellites in the case of SpaceX.

Regardless of how you feel about each of these companies, many of you will end up owning them in your portfolio without even realizing it. Which brings me to…

Changing the rules.

Millions of investors — including us here at Lansing Street — use index funds as a low-cost way to get broad (and sometimes targeted) exposure within a portfolio. These funds track underlying indexes designed to represent a slice of the market. To keep representing that target over time, they periodically rebalance and reconstitute the underlying holdings. Those rules are documented and followed religiously by the index providers.

What we saw with the SpaceX IPO — and expect to see with Anthropic and OpenAI — is that providers are adjusting their rules to accommodate these stocks entering their universe. We expect the Nasdaq 100 (famous for the QQQ ETF), the FTSE Russell 1000, CRSP (closely tied to Vanguard), and MSCI to all include SpaceX shortly after listing. That means investors will hold the stock inside their index funds whether they realize it or not. The main holdout has been the S&P 500, which is standing by its 12-month waiting period and profitability requirements. While I personally don’t love changing the rules for one company — or a handful — there are a couple of nuances worth noting:

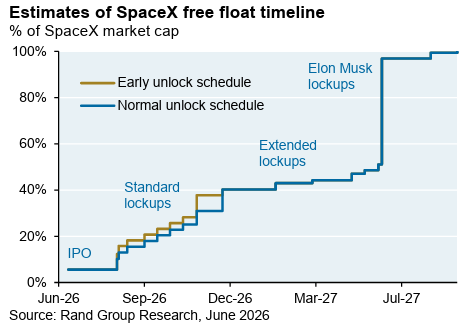

- Free float matters. Because only about 5% of SpaceX trades publicly (the rest is locked up for insiders), the stock’s index weighting will be far lower than its market capitalization alone would suggest.

- Scale is hard to argue with. It’s difficult to make the case against a $1.75 trillion business being included in an index designed to represent the market — and I’d say the same for Anthropic and OpenAI at their valuations.

Should you buy?

I’m going to go out on a limb here and say… it depends. Sorry. The reality is that none of us knows where these businesses — or the overall market — will be in five years. On one hand, SpaceX may have the widest moat (competitive advantage) in public markets right now, and OpenAI and Anthropic are leading providers of large language models in artificial intelligence. On the other hand, the AI industry is still young and these valuations are stretched. Despite what some may think, price does matter.

Over the next twelve months, lockup periods will end for SpaceX insiders, bringing plenty of liquidity to market; we anticipate the same for the other two. The decision to own these companies directly — not simply as part of an index fund — should be made individually, after weighing risk tolerance, time horizon, and overall objectives (a shameless plug for the work the Lansing Street team does over here). Whatever you decide, it’s good to see new equity coming into the markets.